Understanding Hidden Costs of Homeownership

Driving Innovation in Home Equity Solutions

Buying and owning a home is exciting—for most families, their home is the biggest single purchase ever made. It’s not, however, a one-and-done purchase. There are many pros and cons to owning a home, and homeownership means budgeting for more than just a mortgage payment.

The hidden costs of owning a home can add up fast. You’ll have some influence by shopping around or choosing budget options, but factors you can’t control include everything from the rate of inflation to your neighbors’ votes on installing new sidewalks.

Learn about the unexpected costs of owning a home, budgeting for anticipated needs, and identifying when it’s time to sell so you can navigate homeownership expenses with ease.

Initial Purchase Costs

Buying a home comes with fine print under the sale price, and most costs don’t allow you to opt out.

Closing Costs

Both the buyer and seller owe closing costs during a home sale. Although sellers typically pay the buyer’s real estate agent commission, closing costs for buyers average 2% – 6% of the property purchase price. These closing costs include:

- Loan application, origination, underwriting, and credit check fees

- Title search, closing, and administrative fees

- Government recording, title transfer, stamp, and tax service fees

- Prepaid mortgage loan interest covering closing to first monthly payment due date

- Prorated property tax from closing day to end of current payment period

Home Inspection and Appraisal Fees

Before you close on a house, there will be two or three important visits to the property by professionals, all paid by you.

- Home appraisal ($500 – $800 average)1

- Home inspection ($350 average)2

- Wood-destroying insect report if required by lender ($150 average)

Initial Repair and Renovation Costs

Unless you’re buying a new home—or one that was maintained scrupulously—you’re likely to have at least a few projects to complete right away. Repairs and renovations to fund before move-in day often include:

- Repainting and/or removing wallpaper

- Installing different blinds, drapes, or window hardware

- Essential plumbing, electrical, or HVAC repairs if you chose a fixer-upper

- Appliance installation if any are missing

- Carpet removal and wood floor refinishing

Set a budget for materials plus labor for anything that isn’t a DIY job.

Ongoing Ownership Expenses

Separate from your mortgage payment, three of the most common homeownership expenses are insurance, tax, and utilities. None of these have locked-in rates that offer a predictable monthly payment amount over years.

Property Tax

If you own a home in any of the 50 United States, you’ll pay property taxes. Rates vary widely and are voted on and imposed at local levels, although state-wide regulations may restrict local municipalities’ ability to simply increase tax rates to boost their budgets every year.

California’s Proposition 13, for instance, limits property tax rates to 1% of assessed value, limits home value assessments to a 2% increase per year, and establishes a base property value that dates to either 1975 or when the home changes hands.3

In several Mountain West states—Colorado, Wyoming, Nebraska, and Montana—attempts at similar legislation and other approaches to capping property taxes are underway, but it’s unlikely that they can make up revenue needs with anything approaching a Prop 13 mandate.4

The reality is that across most of the United States, property taxes are the major source of funding for schools, streets, libraries, police and fire protection, and more—and as inflation hits their budgets, property tax revenue is the most common solution.

State and Local Property Tax Total

Rates vary widely by location, but here’s a snapshot of how total U.S. property tax revenue has more than tripled over the past 30 years:5

In comparing states, the average effective tax rates (based on what’s actually paid after exemptions rather than raw rates) range from 0.31% in Hawaii to 2.46% in New Jersey. When you break tax rates down to specific counties, they range from 0.15% in Louisiana’s East Feliciana Parish to 3.48% in New York’s Allegany County.6

But it’s not all about the tax rate. Property tax is calculated by multiplying your local tax rate by your home’s value as determined by annual property tax assessments. On average, single-family home property tax rates rose 6.9% last year, the highest annual jump in the past five years, resulting in an average household property tax bill of $2,459 for 2023.7

Remember—your bill is based on the tax rate multiplied by your property value. Values have averaged 4.3% growth from 1991 – 2023, with much higher annual spikes in recent years.8 Like property tax rates, changes in property value vary widely depending on location and other factors.

Your property taxes can also be increased, albeit temporarily, by special assessments for voted-in projects or school levies. On the flip side, property tax reductions are available in some locations through property or personal exemptions such as homestead, military, age, or income status.

Homeowners' Insurance

Property insurance is typically required by your mortgage lender, and optional but strongly recommended if your home is fully owned. It typically provides protection from liability plus property and personal belongings replacement or repair due to damage from:

- Fire, lightning, wind, and hail

- Theft and vandalism

- Visitors’ personal injuries and property damage

The average annual cost of homeowners insurance has increased significantly over the past 4 years:9

- 2021: $1,984

- 2022: $2,123

- 2023: $2,377

- 2024: $2,522

Even more daunting is the annual increase on renewed policies: more than 20% in recent years, compared to about half that in past years.

You can expect that trend of high annual rate increases to continue based on:10

- Less competition, with insurers halting new policies in high-claim, high-regulation states

- Delayed inflation impact as insurance companies face regulatory delays before rate hikes

- Increase in serious weather events leading to more and higher claims and payouts

At an individual level, your best avenue to lower rates may be to work on your credit score—on average, homeowners with poor credit pay 92% more than those with high scores.11 You can also shop around for the best rates, add weather-proofing features to your property that yield premium discounts, and take a close look at your deductible and coverage levels.

Utility Costs

Utility costs rise or fall with the weather, increase over time, and vary between providers when competition exists. To increase predictability, many utility companies will bill you with an annualized average rather than what you actually use each month.

Essentials commonly include:

- Electricity

- Gas or alternate fuel sources

- Water, sewage, and drains

- Garbage and recycling

You can decide whether to include internet, phone, cable, and streaming services under the umbrella of home utilities or a separate budget category.

Home Maintenance and Upkeep

Just like property tax and homeowners insurance rates won’t remain frozen in time, neither will your home itself. The most common reason for loss in property value is lack of maintenance and care.

Regular Maintenance Costs

Maintenance doesn’t mean waiting for something to break—it’s caring proactively for your home and all of its components. Combine seasonal property maintenance checklists, your home inspection report, and identified drips, glitches, and issues to plan a combination of DIY tasks, vendor service calls, and products and materials to update or replace.

Some experts suggest budgeting 1-3% of your current home value based on your climate and your home’s age and building materials.

Unexpected Repairs

Home inspections are vital to uncovering weaknesses and problems, but they’re not a guarantee of zero problems now or in the future. Some aspects of a home are hidden under drywall, carpet, and the dirt itself.

You may need to bear the cost of repairs after a home inspection, such as:

- Foundation cracks or shifts

- Weight-bearing support beam issues

- An early demise of an appliance

- Damage from severe weather, such as ice dams

Landscaping and Exterior Maintenance

Maintenance and upkeep extend to the edges of your property plot. If you’re an avid gardener, you’ll be a step ahead in tending to your home’s exterior. For the rest of us, a seasonal checklist is critical to staying on top of preserving or increasing property value.

Seasonal Landscaping Tasks

Replacement Costs

The good news about home system and appliance breakdowns is that you can loosely plan for when you’ll need to be ready to replace them. Along with individual warranties and product documentation, the International Association of Certified Home Inspectors offers an inclusive set of lifespan expectancies for everything from poured-concrete foundations (100+ years) to carbon monoxide detectors (five years).12

Appliance and System Lifespans

There are very few components beyond the foundation or structural elements that you can expect to last a human lifetime. Ideally, you’ll enter into a home with complete records of the installation date of each major appliance and a record of property repairs and improvements—and add to this documentation as you complete work.

This information is key to planning ahead. You can compare it to expected product and material lifespans to map out what you may need to replace each year. Bear in mind these are estimates only—it’s possible that you’ll install a dishwasher that may need to be replaced after the first few years or luck out with a water heater keeping it hot for three decades.

Lifespan of Major Home Appliances and Systems

oven

ange

Costs of Replacements and Upgrades

Review your property needs annually, including checking on items nearing the end of their useful lives. With attentive maintenance, they may outlive expectations, but consider safety inspections, have a service provider selected, and check on current sale prices.

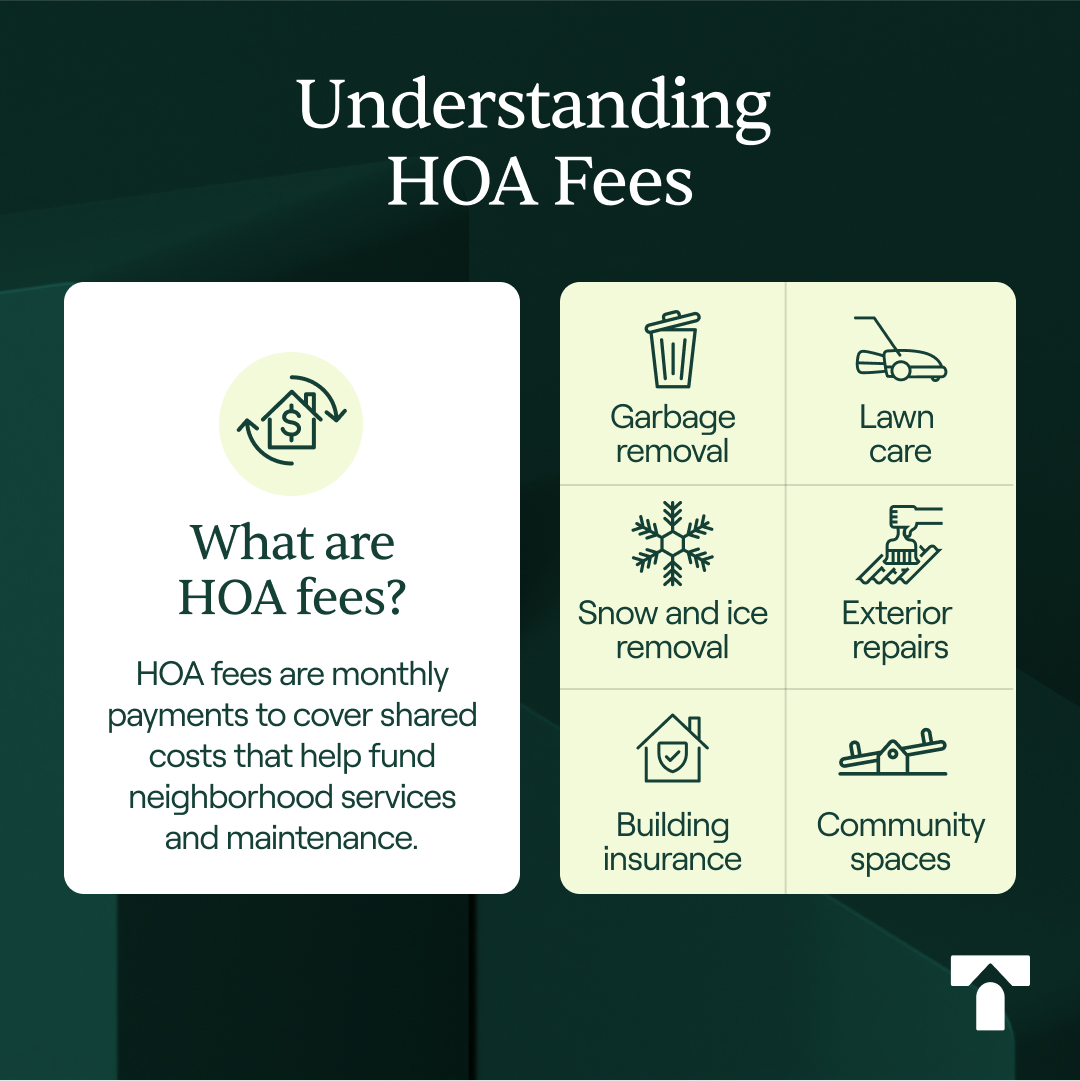

Homeowners Association (HOA) Fees

If you buy a home in a common interest community (CIC) then you’ll need to budget for monthly HOA fees and the possibility of special assessments.

Understanding HOA Fees

HOA fees are a way for neighborhoods to pay into a central fund used to cover common costs. Although complaints about HOA overcontrol or mismanagement abound, the concept is fiscally sound—bargaining for lawn care for 30 adjacent homes will take less time and cost than each of those 30 households finding their own providers.

Services paid by HOA fees often include:

- Utilities such as garbage removal

- Lawn care

- Snow and ice removal

- Repairs and maintenance on some exterior features

- Exterior building insurance coverage and maintenance for multi-unit structures

- Community spaces and services

When you consider a home in a CIC, you’ll be provided the HOA rates to evaluate before making an offer, but just like most homeownership expenses, they’ll increase over time. Fees are usually evaluated and adjusted annually by a governing board.

Be sure to check out the HOA bylaws and your state’s laws. Ask:

- How often fees can be increased—annually, or two or three times per year?

- How much notice is required before a fee increase?

- Who has control over increases—is a vote required, or the board alone?

- Are there limits on the size of an increase?

Average 2024 monthly HOA fees range from $300 – $400 in most states, hitting $448 in Arizona, $469 in Missouri, and $653 in New York City.13,14 Most residents, however, can expect rate hikes based on inflation. In a recent poll of HOA board members and CIC managers, 71% plan to increase fees—and 19% of that number plan on an increase of 11% – 25%.

Special Assessments

HOA fees usually cover basic, ongoing home maintenance and a limited reserve fund—they don’t stockpile dollars for big projects. Special assessments are used when the CIC requires a major renovation or repair, such as new roofs, sewage drain repairs, or repaving drives.

This could either be a one-time cost or an addition to your monthly HOA fees over a period.

Property Value Fluctuations

When it comes to the actual value of your property, you can’t truly know it down to the penny until you sell it. Current market value, then, acts as an informed estimate of what your home would be sold for at the time of valuation.

This estimate is based on:

- Analyzing data and historical trends to understand what provides intrinsic value

- Understanding how much buyers can afford and will pay

- Balancing the many factors that influence buying decisions

Although you can manage value related to the maintenance and improvement of your property, there are some factors—like market change and local economic conditions—that you’ll need to be aware of but cannot significantly influence.

Market Impact

What can most buyers afford based on today’s socioeconomic conditions? Whether you plan to remain in your home or list it, interest rates, inflation, and other market conditions impact its value.

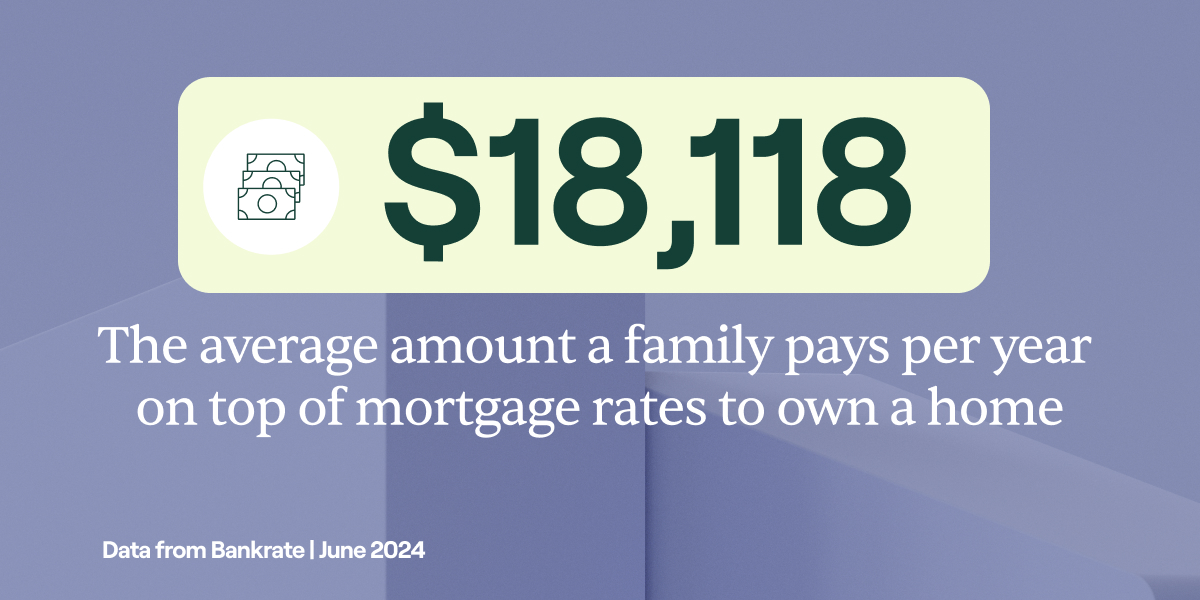

Median home prices in the United States rose by nearly 28% over the last five years, from $322,500 in 2019 to $412,300 in 2024.15 In that same time frame, the average interest rate of a 30-year fixed-rate mortgage rose 80% from 3.6% to 6.49%.16

The COVID-19 pandemic had an enormous effect on the housing market. With both their work and entertainment time migrating to the homefront, a staggering number of families opted to:

- Level up to larger homes

- Head for destination cities

- Migrate from a metropolis to a lower cost-of-living community

With labor restrictions and supply chain disruption limiting new construction, housing demand outpaced supply, home values soared, and buyers had cash from reduced entertainment and consumer spending plus a series of government payouts, all while mortgage interest rates dropped to a historical low.17

Now, the prime rate has nearly doubled and home prices have slowed or stopped but not returned to pre-pandemic levels in most markets. Using the median house prices and average interest rates above, purchasing a house would require:18

- $64,500 downpayment and $1,173 monthly mortgage payment in 2019

- $82,460 downpayment and $1,500 monthly mortgage payment in 2024

The effect of high home prices in your location plus high interest rates is that your home is less affordable, and your pool of potential buyers is smaller. Remember, current market value equals the price your property could realistically demand at a given time—which means market conditions can determine whether your property value grows, stalls, or falls.

Plus, rising inflation doesn’t stop at the grocery store—it ripples through most aspects of service and product pricing, including the dollar value of homeowners insurance, property tax, agent commissions, and building materials and labor. That means higher prices for you as a homeowner plus a potentially lower property value based on higher competition for fewer buyers.

Local Economic Conditions

Both the national and local news can influence property value. New developments, infrastructure changes, and business openings or closures can factor into your home’s value. Employment level, in particular, is a critical measurement of whether potential buyers are entering your area (value increases) or more homeowners are looking to sell and leave (value drops).

Local Changes

Long-Term Financial Planning

How can you ensure you can afford the ongoing homeownership costs beyond your mortgage payment? It takes a combination of financial planning for known costs and saving emergency funds to help with the unexpected.

Budgeting for Hidden Homeownership Costs

Start by tracking the age and condition of your home systems, appliances, and surfaces. Plan out a year-by-year map of replacements and upgrades using InterNACHI's Standard Estimated Life Expectancy Chart for Homes.13 Expectancy isn’t a guaranteed outcome, but it can help you anticipate likely costs within the next one, five, ten, and twenty years.

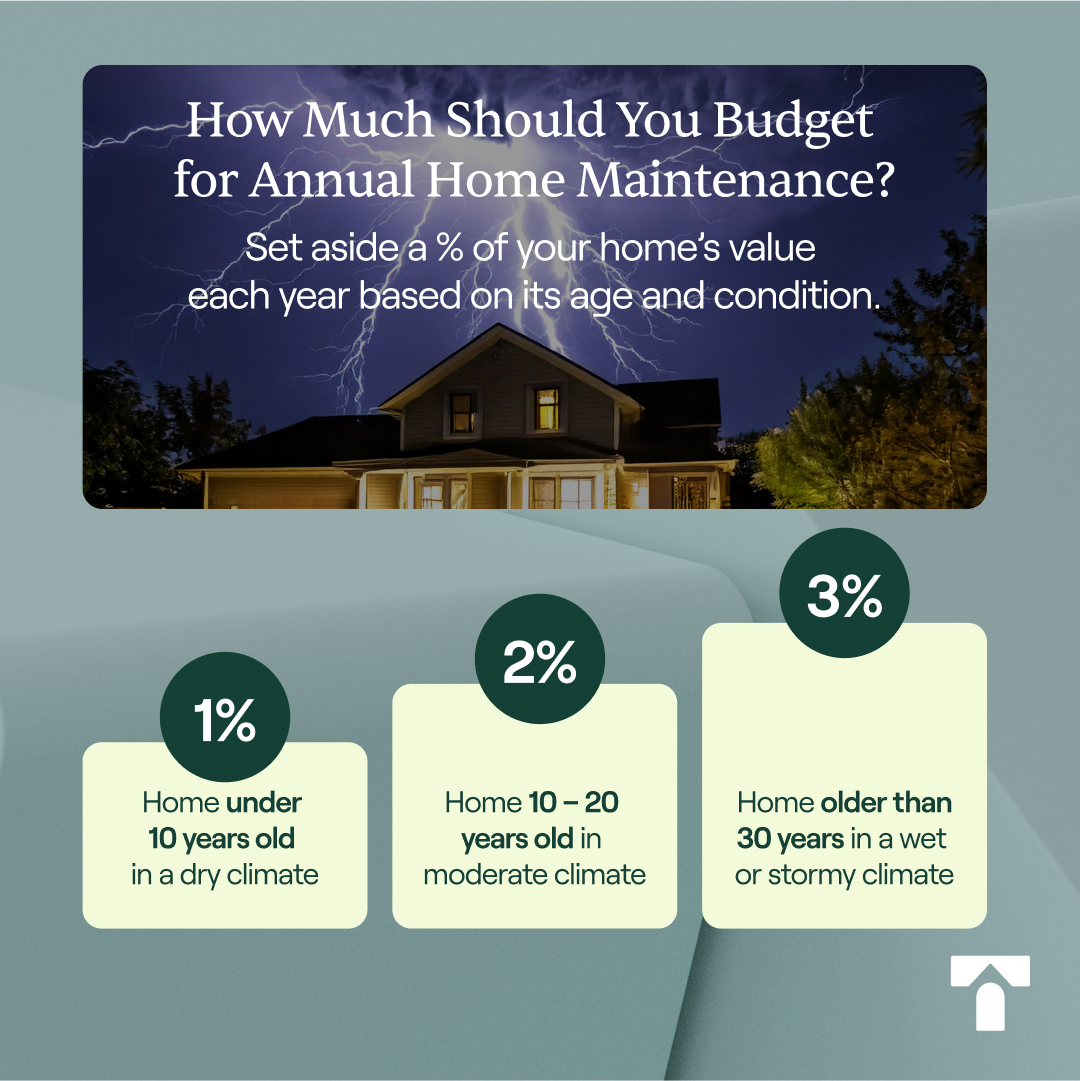

In terms of annual budgeting, consider a percentage-of-property-value approach for ongoing maintenance. To calculate how much to set aside for the year, match your home’s characteristics below and multiply the percentage by the current property value:19

- 1% for a home under 10 years old with durable materials in a dry climate

- 2% for a home 10 – 20 years old with moderately durable materials in moderate climate

- 3% for a home older than 30 years with lower-life materials in a wet or stormy climate

Climate Change Impact

While the U.S Department of the Treasury’s recent Impact of Climate Change on American Household Finances report doesn’t offer up figures, it does explore multiple ways that weather changes can hit the American wallet at a household rather than government expenditures level.20 These include:

Insurance Premiums

The U.S. categorizes extreme-weather events that affect people's lives and livelihoods as “billion-dollar disasters,” and the number per year is on the rise:21

- 8.5 events per year on average from 1980 – 2023

- 20.4 events per year on average from 2019 – 2023

- 28 events in 2023

For households, this means higher premium costs, which will be compounded by less competition.

Insurance is state-regulated, with some states holding tight rein over premium prices and policy coverage. Many companies have either stopped writing new policies or doing business entirely in California, Florida, Georgia, South Carolina, New Jersey, New York and Arizona, where the intersection of higher claim numbers/payouts and government price controls has removed profit potential.

Utilities

Heat waves and higher average temperatures mean more fuel for air conditioning in central and southern states. It may also mean installing or using more air cooling systems in upper floors, attics, garages, or secondary units.

Repairs and Upgrades

Damage from extreme weather events and severe everyday weather can shorten the lifespan of building materials, systems, or appliances. Your roof, siding, exterior paint, landscaping, and walkway or driveway surfaces may need more frequent repair or replacement.

You may also find it advisable to upgrade components that protect against severe weather such as storm-resistant shutters and windows, both for safety and to potentially lower your insurance premiums and reduce out-of-pocket costs after weather damage.

Importance of an Emergency Fund

While you can take your time solving some property issues, others are essential to survival or critical to fix before they lead to a worse—and more expensive—problem. An emergency fund is often recommended in terms of a safety net for unexpected job loss, but it also serves as protection against the unexpected for homeowners.

Three to six months’ worth of total monthly expenses is a common goal overall, or you can set aside the aforementioned 1-3% of property value separately for a dedicated home emergency fund.

Exiting Homeownership

If you’re doing the math and leaning away from homeownership, what are your choices? The three top options are:

Sell Your Home

If you’re ready to head off into the horizon (or move across town) then it might be time to sell. For most sellers, this means engaging a real estate agent to list and market your home after helping you price it and decide what changes or improvements to make to maximize profits.

There are many factors that determine how long a traditional sale takes—location, features, local market conditions—but on average, U.S. homes currently spend:

- Up to six months getting the property ready to sell22

- 50 days on the market in mid-summer to a 69-day peak in the winter23

- 43 days from offer to closing

Rent Out Your Property

Have you considered turning your home into a rental property? While leasing it out doesn’t erase the ongoing costs of homeownership, it can shift them from personal to business costs. So long as your lease rate covers the mortgage payment, lease management services, and repairs and maintenance, any extra becomes profit, plus you’ll have a long-term investment that pays off with a future property sale.

Challenges include:

- Gaps in renter occupancy

- More wear, tear, and damage from renters vs. owners

- Either the headache of managing the property yourself or the extra cost of hiring it out

Sell and Stay Transaction

How about continuing to live in your home but gaining freedom from homeownership costs and hassles? You could sell your home and then sign a lease agreement to remain on as a tenant.

For some homeowners, this is the best of both worlds, offering:

- No more mortgage debt

- Cash-out of your home equity

- No property tax or property insurance

- A landlord who takes care of essential repairs

Instead of saving every dime for plumbing repairs or a new roof, you’ll have cash in hand to use for retirement, a new business, paying down high-interest credit cards, or whatever your family needs.

Homeownership Isn’t for Everyone

In tandem with the initial price tag, buying a home comes with hefty hidden expenses that you can’t fully predict or control. There are property tax, insurance, and HOA fees, costs for labor and materials for maintenance and repairs—including the potential for massive structural, infestation-related, and system replacement issues—all of which continue to increase in price.

The fact is, homeownership can be more of a drain on resources than an ideal living situation for some. If you’re looking for minimalism in your budget, lower stress, and more control over monthly housing costs, a sell and stay transaction may be the right fit for you. It helps you streamline costs and responsibilities without the expense and hassle of moving, freeing you up to live a happy, healthy life in the security of the home you love.

Truehold can help you stay in your current home without the burden of property tax, property insurance, or essential repairs. Plus, you’ll pay off your mortgage debt and potentially gain financial freedom when you unlock your equity.

Sources:

- Nerdwallet. Mortgage Closing Costs: How Much You’ll Pay. https://www.nerdwallet.com/article/mortgages/closing-costs-mortgage-fees-explained

- Bankrate. How much does it cost to sell a home? https://www.bankrate.com/real-estate/how-much-does-it-cost-to-sell-house/

- Santa Clara County Assessor's Office. Understanding Proposition 13. https://www.sccassessor.org/faq/understanding-proposition-13

- Pew. As Property Tax Bills Rise, States Look for Long-Term Solutions. https://www.pewtrusts.org/en/research-and-analysis/articles/2024/04/25/as-property-tax-bills-rise-states-look-for-long-term-solutions

- FRED. Personal current taxes: State and local: Property taxes (S210401A027NBEA). https://fred.stlouisfed.org/series/S210401A027NBEA

- The Motley Fool. Property Taxes in Each State.https://www.fool.com/research/property-tax-rates-by-state/

- Bankrate. Property tax rates by state: What to expect in your area. https://www.bankrate.com/real-estate/property-tax-by-state/

- Rocket Mortgage. Home Appreciation: What Does Appreciation Mean And How Is It Calculated? https://www.rocketmortgage.com/learn/home-appreciation

- Insurify. Report: Home Insurance Rates to Rise 6% in 2024 After 20% Increase in Last Two Years. https://insurify.com/homeowners-insurance/report/home-insurance-price-projections/

- Money. How High Could Home Insurance Rates Jump This Year? Here's What Experts Predict. https://money.com/home-insurance-rates-predictions-2024/

- Bankrate. Average homeowners insurance cost in August 2024. https://www.bankrate.com/insurance/homeowners-insurance/homeowners-insurance-cost/

- InterNACHI. InterNACHI's Standard Estimated Life Expectancy Chart for Homes. https://www.nachi.org/life-expectancy.htm

- DoorLoop. HOA Statistics for 2024 - Making Sense of Benchmarks. https://www.doorloop.com/blog/hoa-statistics

- RubyHome. HOA Stats: Average HOA Fees & Number of HOAs by State (2024). https://www.rubyhome.com/blog/hoa-stats/

- FRED. Median Sales Price of Houses Sold for the United States. https://fred.stlouisfed.org/series/MSPUS

- FRED.30-Year Fixed Rate Mortgage Average in the United States.https://fred.stlouisfed.org/series/MORTGAGE30US

- Bankrate. How did COVID affect the housing market? https://www.bankrate.com/real-estate/covid-impact-on-the-housing-market/

- Investopedia. Mortgage Calculator. https://www.investopedia.com/mortgage-calculator-5084794

- The Balance. How Much To Budget for Home Maintenance. https://www.thebalancemoney.com/home-maintenance-budget-453820

- U.S Department of the Treasury. FACT SHEET: The Impact of Climate Change on American Household Finances. https://home.treasury.gov/news/press-releases/jy1775

- Climate.gov. 2023: A historic year of U.S. billion-dollar weather and climate disasters. https://www.climate.gov/news-features/blogs/beyond-data/2023-historic-year-us-billion-dollar-weather-and-climate-disasters

- Zillow. What Is the Average Time to Sell a House? https://www.zillow.com/learn/average-time-to-sell-a-house/

- HomeLight. How Long Does It Take to Sell a House? (2024). https://www.homelight.com/blog/how-long-does-it-take-to-sell-a-house/

Driving Innovation in Home Equity Solutions

Truehold’s team is located across the US, working to help homeowners and investors access their hard-earned wealth. If you’re interested in joining our mission-driven organization, reach out to careers@truehold.com