Since financial planning is a tedious process, you may benefit from creating a checklist. Learn how to stay on top of your financial goals with these tips.

Personal/family financial planning—is this a phrase that makes you wince? From complex Excel spreadsheets to the pros and cons of IRAs, personal finances and wealth management can quickly become whirlwind topics that have your head spinning.

The good news is that following a financial planning checklist is a fairly straightforward way to stay on top of your financial life. Plus, once you have your goals, budget, and plan set up, it’ll be easier to stay on top of your progress and ensure you’re on track to meet your family, professional, and personal financial goals.

By visualizing the destination of your financial situation before you begin your journey, you can break down long-term goals into incremental steps—slowly walking your way to your dream financial state. Below are some common financial checklist goals to consider, but if yours is to buy up a deserted town and turn it into a Wild West theme park, then by all means add that.

Once you have your financial plan laid out, add notes on timeline and priority. What is a next-three-month project versus a maybe-in-ten-years goal? Which do you consider critical, and which would be nice but not necessary? This process will help incorporate your short- and long-term financial decisions into a budget and savings plan.

Time to gather up your paper and electronic files. You’ll want to pull together:

Also gather current statements for debts, including:

You’ll use these documents to populate your budget and evaluate your savings and insurance holdings.

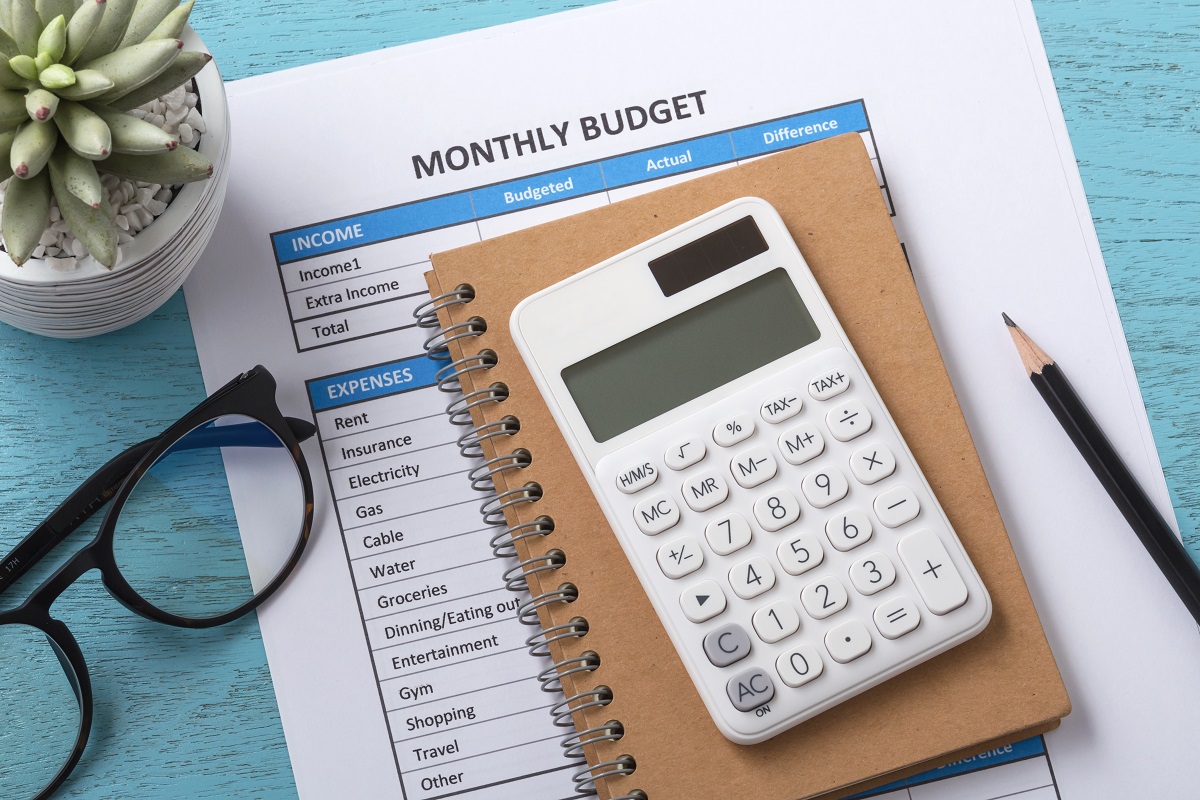

A budget is a window into your spending and a tool to help you accomplish your financial goals. There are four main elements of a budget:

When you keep a budget updated, you’ll be able to see how you’re allocating your money, debt, and savings over time.

So how do you start a tracking budget? You can set up your own spreadsheet or download a premade budget template, or use a free or low-cost mobile budgeting app. Try a few out and see what’s most helpful for you. Remember, the best tool is one you’ll actually use, not one that’s tricked out with every bell and whistle but is too overwhelming to stay on top of.

A savings plan is a strategy to help you identify what amount of savings you need, and then to actively save money for financial success. Top of the list for most financial advisors is your emergency savings.

An emergency fund is intended to cover:

Because it needs to be available at short notice, an emergency fund should be liquid—cash you can get your hands on, versus money tied up in stocks, bonds, or long-term certificates of deposit. A high-yield savings account or money market account is ideal.

So how much do you need? Ideally, an emergency fund should equal saving three to six months’ income, but if you’re just starting out, aim for a goal of $1,000.

If you’re ready to throw in the towel, don’t panic—you’re not alone. A January 2022 survey showed that 56% of Americans wouldn’t be able to cover a $1,000 emergency expense with their savings.1 Take a breath, and consider these tips:

Just as with emergency funds, Americans tend to fall behind on retirement planning—only 36% are on track for retirement savings, and 25% have nothing saved, per a 2021 study by PwC.2 The good news is that it’s never too late to start saving for your retirement plan. Some goals worth considering include:

How much will you need in retirement savings? There are many calculations out there, such as:

To identify retirement income goals, consider:

The first thing you need to figure out is whether your debt is from major purchases, such as a house or car, or from lifestyle spending. Secondly, are you staying on top of debt repayment on a monthly basis, or is it growing as you scramble to make minimum payments?

If high-interest or rolling debt is a concern, consider speaking with a non-profit credit counseling organization. They can provide free information and guidance on managing debt, negotiating with creditors, and whether you may want to consider debt consolidation.3

Once you’ve summarized your financial picture, use details and documents to identify savings opportunities. Did you shop around once and then never revisit cost comparisons? Look into:

Your budget won’t help much if you only fill it in once. On a monthly basis:

On an annual basis, review this checklist with the goal of ensuring:

Your financial plan isn’t a “set it and forget it” situation—it will change over time based on your shifting goals, needs, and resources.

Converting your home equity to cash can fund trusts that will generate monthly income, provide the money needed for to pay off debt, build or buy a new home, secure your retirement, or help you fund your dream lifestyle.

If a house sale hasn’t been on your radar because you have no interest in moving, consider Truehold's sell and stay transaction, an alternative that allows you to unlock your equity without leaving your home.

Sources:

1. CNBC. 56% of Americans can’t cover a $1,000 emergency expense with savings. https://www.cnbc.com/2022/01/19/56percent-of-americans-cant-cover-a-1000-emergency-expense-with-savings.html

2. PwC. Retirement in America. https://www.pwc.com/us/en/industries/financial-services/library/retirement-in-america.html

3. Money Crashers. 5 Different Types of Savings You Should Have Right Now. https://www.moneycrashers.com/types-savings-emergency-retirement-personal/

4. Consumer Financial Protection Bureau (CFPB). What is credit counseling? https://www.consumerfinance.gov/ask-cfpb/what-is-credit-counseling-en-1451/

Chat with a real person & get an offer for your home within 48 hours.

Call (314) 353-9757.jpg)

.jpg)

.jpg)